We are in the third quarter of 2017 and deal data is now available through the end of the second quarter of 2017. In this report, we review our region’s most active industry sectors and give an outlook for the remaining 2017 year.

Analysis by Sector

These 7 industries are among the most active sectors that drive M&A activity in our region:

i. Aerospace

ii. Chemicals

iii. Construction and Engineering

iv. Energy: Oil and Gas

v. Healthcare

vi. Manufacturing

vii. Transportation, Logistics, Distribution

M&A Transaction Report and Outlook by Sector

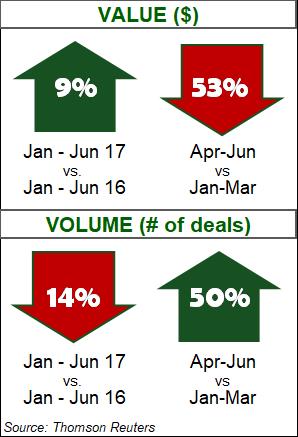

I. Aerospace

Although a relatively slow quarter, value is up over the first six months of 2016.

Highlights:

Highlights:

- With the current Administration’s proposed increase in defense spending, the opportunities look encouraging for the industry. A strong economy also drives a positive outlook.

- There were five megadeals announced this quarter, accounting for a majority of deal value.

- The Aircraft & Parts category made up just under half of deal value and near a quarter of deal volume this year. Military Arms & Vehicles and Electronic Equipment are the two other categories with strong contributions.

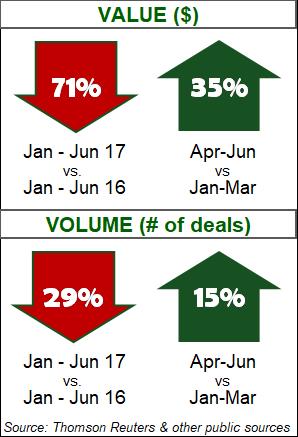

II. Chemicals

Strategic investments remain steady in the second quarter.

Highlights:

Highlights:

- While battling lower demand, the industry continues to turn to consolidation to increase market share, identifying synergies and reducing operating costs.

- Three megadeals accounted for a majority of transaction value, with the Huntsman/Clariant merger producing half of deal value.

- Specialty Chemicals leads M&A activity this quarter, with 48% of transactions and 78% of deal value.

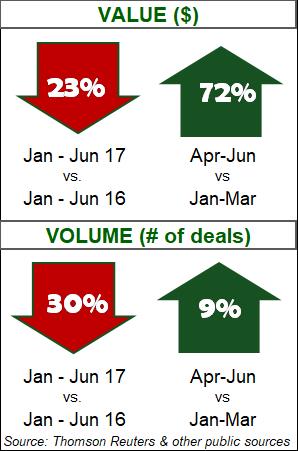

III. Construction and Engineering

Increase in deal value is primarily credited to a sluggish first quarter.

Highlights:

Highlights:

- Civil Engineering accounted for 29% of total deal value, while Construction Materials Manufacturing comprised 23% of total deal value year to date. A rise in infrastructure and utility construction projects explains the activity in these categories.

- Four megadeals comprised 45% of deal value this quarter, with one of those accounting for 24 % of deal value.

- The number of larger transactions may indicate companies moving past the uncertainty of the last two quarters, while the reduced volume of activity may point to ongoing uncertainty as acquirers wait for legislative action proposed by the Trump administration earlier this year.

IV. Energy: Oil and Gas

Compared to an extraordinary first quarter, values in Q2 have declined; however, this was still the third highest Q2 in deal value over the last eight years.

Highlights:

- Shale deals made a 124% year over year increase in deal value. The Permian basin was the most active in the second quarter, with the Marcellus, Eagle Ford and Niobrara generating the remainder of deals.

- The upstream market had the highest number of deals with 58% of the total, followed by midstream with 26%, and downstream and oilfield services with 8% each.

- Megadeals led deal activity with 78% of first half deal value.

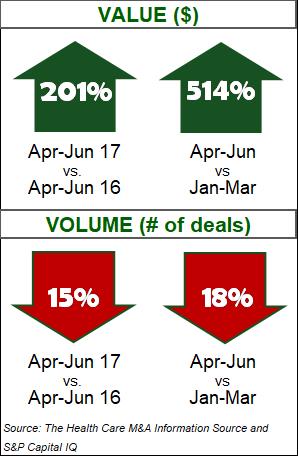

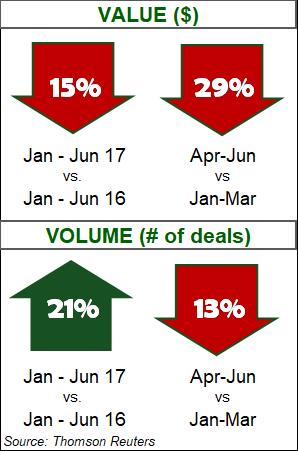

V. Healthcare

Amidst uncertainty with Congress and the current Administration, high value deals continue to move forward.

Highlights:

Highlights:

- The Congressional Budget Office predicts health costs will continue to increase based on the aging population, greater healthcare spending per person, and the Affordable Care Act (or any other potential substitute).

- With increased use of electronic health record systems to improve efficiency, hospitals continue to invest in IT security software and cybersecurity.

- Ten megadeals account for the rise in deal value. The LongTerm Care sector was the most active in terms of volume with 34% of the deals. Healthcare Services dominated at 71% of deal value.

VI. Manufacturing

With political uncertainty, the industry remains subdued.

Highlights:

Highlights:

- Industrial Manufacturing dealmakers face adversity with continued uncertainty from the US Administration regarding trade, regulatory environment, and tax reform.

- While this has sidelined some investors, the increase in volume has analysts convinced that strategic acquisition growth will remain a priority.

- Industrial Machinery was the highest volume category this quarter, with Rubber & Plastic Products second.

- Without a catalyst, such as tax reform, the industry may remain subdued through the remainder of 2017.

VII. Transportation, Logistics, Distribution

The industry bounced back in the second quarter to record the highest quarterly value and second highest deal volume in three years.

![]() Highlights:

Highlights:

- Due to Atlantia SpA acquiring Abertis Infraestructuras SA, the Passenger Ground category accounted for 47% of deal value. Shipping accounted for 29% of transaction volume.

- Trucking realized the highest quarter-over-quarter growth in number of deals.

- Shipping and Logistics both realized their largest volume of deals over the past three years. Strong M&A activity in the Logistics sector has accompanied increased growth in the Shipping sector as both respond to structural changes in the industry.

- Seven megadeals accounted for about 63% of the total deal value for the quarter.

How Can ClearRidge Help You Sell Your Business?

Clients trust ClearRidge to deliver a confidential and discrete preparation and sale process, to remove obstacles to close a transaction and ensure only the best prospective buyers make it to the closing table, with the capital and commitment to close a transaction. The ultimate goal is a higher sale price and preferential deal terms.

ClearRidge is the most active M&A advisory firm in our region and has been recognized for the quality of our work and success at managing and arranging transactions for our clients’ companies. For further information on our team, industry expertise and transactions history, please visit www.ClearRidgeCapital.com.

Sources: This report has been compiled from reports and research including federal data, independent analysis, Reuters, CFA, Janes Capital Partners Sources, PCE-Companies, Kiplinger, Mergermarket, PricewaterhouseCoopers, and SDR Ventures.

Note: In the report, you will see that some of the deal data is for larger public companies. The most reliable and timely data tends to be for the larger companies in each industry; however, deal activity of largest corporations is also a good barometer for M&A activity among midsized companies in the same industry.